Disposable income is the money an individual or household has to save or spend after taxes. Discretionary income is what is left after necessary expenses are deducted from disposable income. These two types of income can affect the way consumers spend or save.

In economics, the relationship between income and expenses is measured by the marginal propensity to consume (MPC). It is a measure of how expenses change in response to changes in income. It is typically shown as a relationship between income and expenses (see Figure 1), and it falls between 0 and 1. As a general rule, income and expenses tend to increase over time.

The steepness of the slope in the consumption vs income graph depends on the percentage of new income that is spent versus the percentage that is saved. For instance, if an individual spends 50 cents of every additional dollar they earn, their MPC would be 0.5 (slope of the graph). The MPC can be used to understand how changes in income affect an individual’s spending and saving habits.

The MPC is typically higher for lower-income individuals than for higher-income individuals, as higher-income individuals are more likely to have met their consumption needs. A related measure is the marginal propensity to save (MPS), which is calculated as 1 – MPC. This reflects the fact that every dollar not spent is saved.

In our recent showcases, we discussed topics such as our ideal customer and the reasons behind it. As we are in the investing business, understanding our users’ savings and expenditures is crucial. Time is a significant factor in investing, and I recently started researching how the tendency to save money (propensity to save) changes with age.

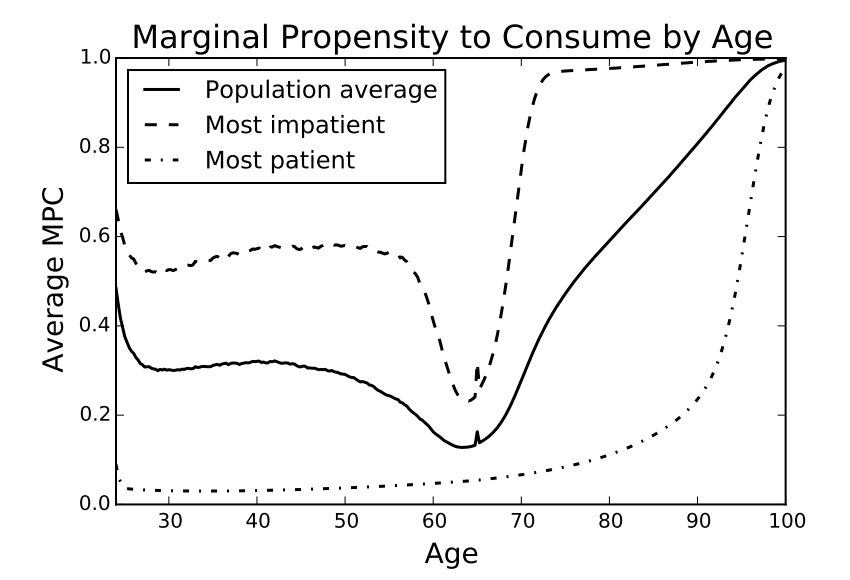

When individuals are in their early 20s and have just started earning income, their marginal propensity to consume (MPC) is typically high due to their low income levels (see Figure 2 for how the aggregate MPC of a sample group varies with age).

The MPC then decreases until an individual reaches their mid to late 20s, then gradually increases until they are in their 40s. This is because people typically take on more responsibilities and upgrade their lifestyles as they get older. Later, the MPC drops drastically around the time of retirement, as retirement funds become available for spending but have not yet been used. After this point, the MPC may increase again, but the exact trajectory can vary depending on the individual.

How does this help us? Here are a few examples.

- In general, MPCs are low around late twenties to early thirties, this is our ideal customer profile (ICP) based on age. We concluded this in our showcase as well. We need to target and acquire more of these individuals.

- The fact that patient consumers tend to have relatively lower and constant MPCs throughout their earning years can be useful in terms of communication. This may involve highlighting the long-term benefits of investing.

- Interestingly, our ideal customers are likely to have parents who have recently retired or are about to retire. These parents’ MPC levels are the lowest (refer to figure 2). By tailoring our messages to this specific audience, we may be able to attract more investments from the entire household.

If you’d like to discuss more on this topic or have any suggestions, do reach out to me. Cheers!